JACKSONVILLE, Fla. — It'll cost you more to get a loan right now, but the federal interest rate hike has good intentions.

The Federal Open Market Committee is trying to curb inflation.

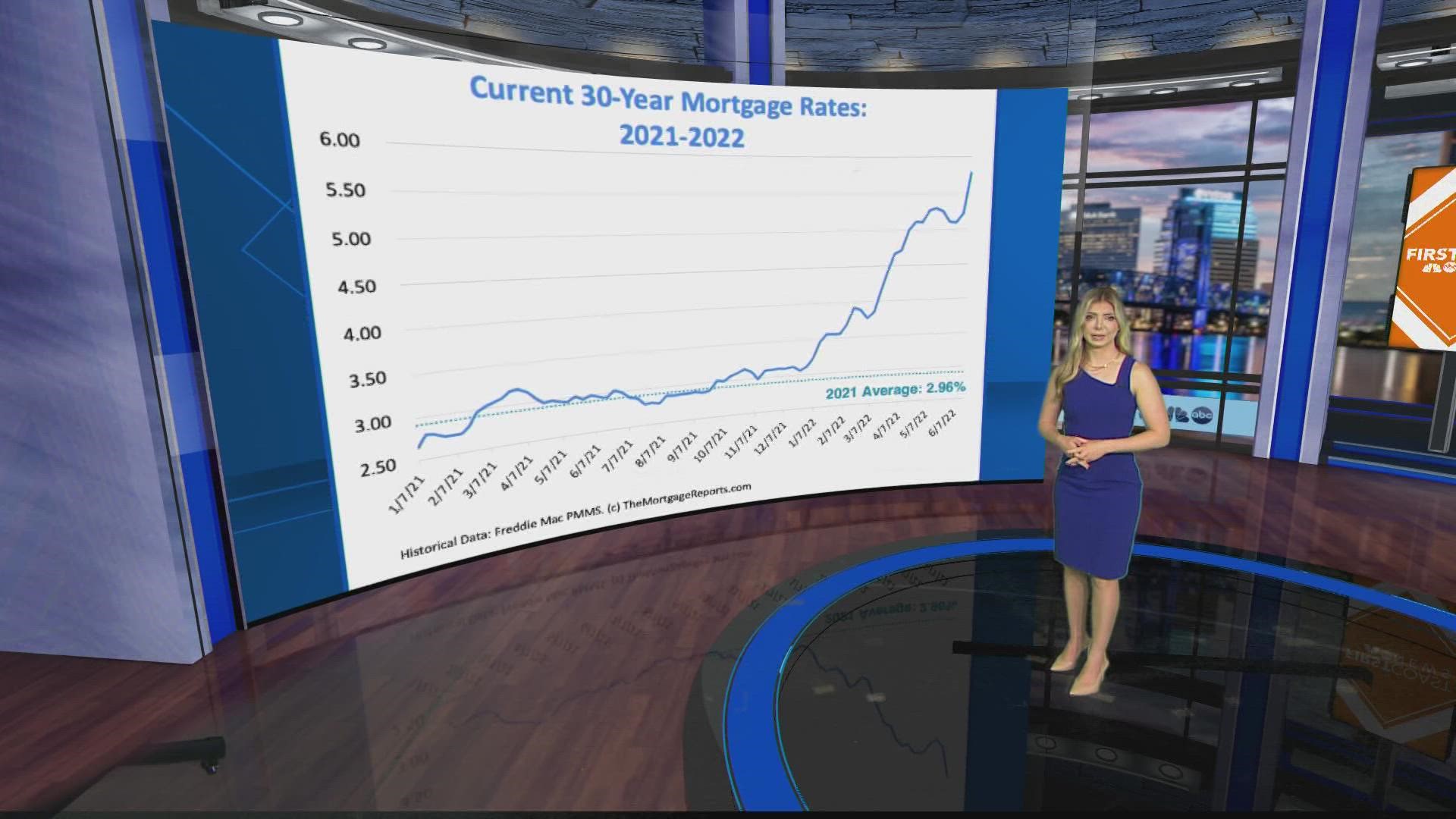

Interest rates have climbed to around 5 percent for mortgages from around 3 percent just in January. Mortgage Operations Manager at Jax Federal Credit Union Stephen Solliday says that means you will pay more over time in interest and it is affects what home you can now afford.

The rate hike increases what your monthly mortgage payment would be and that will set back potential home buyers.

So make the most of your money in the meantime by saving, but not in a normal savings account. Try a:

• High yield savings: I'm finding interest rates as high as 1.61%.

• CD: I found interest rates at 2.5% for 18 months. That means you can't touch the money for that period of time, but your interest will accumulate.

• Money market: I've seen an interest rate at 1.61%.

Check out bankrate.com or nerdwallet.com to see which accounts have the best rates right now.

Savings account interest rates are the good kind. That's the percentage the bank pays you based on how much money you have in your account.

If you have time to kill, you can wait to buy a home and save more but Solliday says it's still not a BAD time to buy.

"(Interest rates) can adjust down as quickly as they adjust up if the market calls for it. It's important to keep in mind, too, this time last year rates were at an absolute historic low," Solliday said. "So even though we've had historic increases this year, it doesn't mean we've gotten to historic highs at all. We're kind of in a midpoint right now."

He says when interest rates drop, you can refinance your home and get a better rate later on.

If you're already a homeowner, you may have a chance to get rid of credit card debt.

The interest hike also impacts your credit card debt.

Solliday says you can take out a home equity loan and use it to pay off your credit card debt. According to CreditCard.com, the average interest rates for credit cards right now is around 17% and it will rise. Whereas a home equity loan is around 5%.

Solliday says don't let all of this worry you.

“It’s kind of been a taboo thing since 2008, whereas the interest rate hike really does signal confidence in the job market and economy, too," Solliday explains. "They can’t raise rates unless jobs are filled.”

Unemployment rates nationwide is the lowest it's been since February 2020.